Jeff Hales, PhD, Chair of the SASB Standards Board

For some weeks now, I’ve been preparing for a new semester. That means getting ready to teach a new batch of energetic accounting students about the importance of – not debits and credits – but of conceptual frameworks. That may be surprising to some, but it shouldn’t be. Accounting may be the language of business, but, as I tell my students, conceptual frameworks are the language of accounting.

As a student of conceptual frameworks, I’m convinced that these frameworks aren’t just esoteric pontifications. Instead, they play two crucial roles for accounting standard setters. First and foremost, they provide an intellectual grounding in core principles and objectives that guide standard-setting efforts. Second, they provide a common set of language that improves the ability of a standard setter to communicate ideas and intentions – both internally within the organisation and externally when engaged with key stakeholders as part of a transparent, market-informed, standard-setting process.

If that type of conceptual clarity is important when discussing the likes of revenues and expenses, it is no less needed when discussing the components of sustainability information. That’s why I’m excited that, over the course of the past year, the Standards Board at SASB has been focusing on strengthening two key governance documents: our Conceptual Framework and our Rules of Procedure.

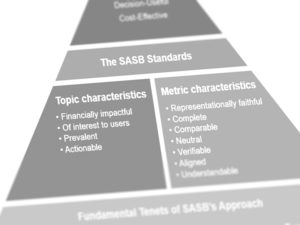

The Conceptual Framework sets out the basic concepts, principles, definitions, and objectives that guide the Standards Board and technical staff in our approach to setting sustainability accounting standards. The Rules of Procedure establishes and describes the policies and practices followed by the Standards Board in developing, issuing, and maintaining the SASB Standards. Together, these complementary documents are important in guiding the Standards Board and in communicating to you who SASB is, what the Standards Board does, and how we do it.

The revised Conceptual Framework and Rules of Procedure documents are now available on SASB’s website for review and public comment. We hope you will share your comments, questions, and concerns as you read through each document. While the Standards Board is not fundamentally changing our approach to sustainability accounting or to the processes we use to conduct standard setting, we have tried to more clearly and effectively communicate those key concepts. And, because communication is a two-sided endeavor, it’s important for us to know how the words and concepts we use are understood by you, our key stakeholders.

To learn more about proposed revisions and how to provide feedback, register for a webinar on September 10, 2020.

Jeffrey Hales is the Charles T. Zlatkovich Centennial Professor of Accounting at the University of Texas at Austin and the Chair of the Sustainability Accounting Standards Board.